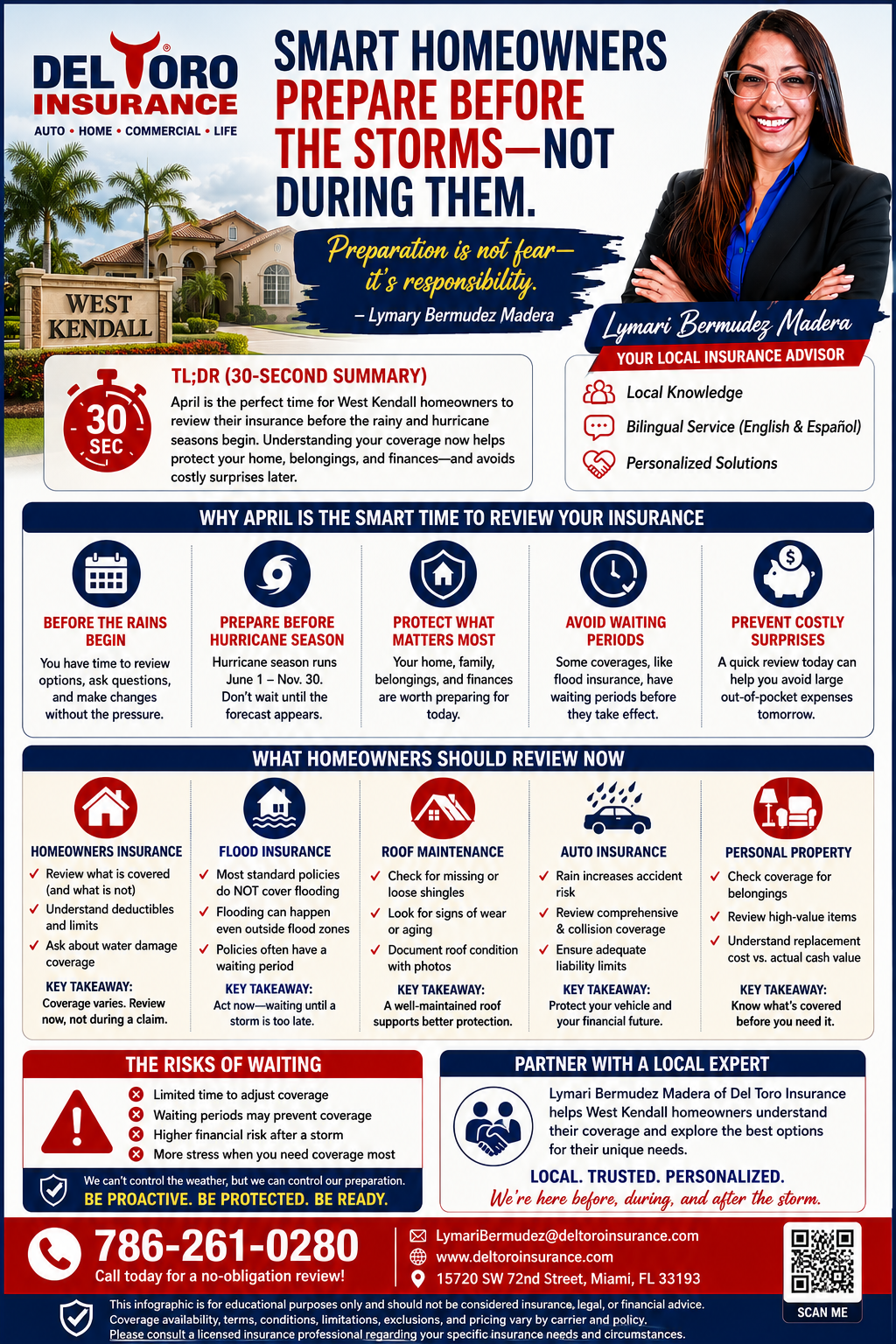

Why Should West Kendall Homeowners Review Their Insurance Before Hurricane Season?

Smart homeowners prepare before storms arrive, not after they appear on the forecast.

Preparation creates confidence when uncertainty arrives.

– Lymari Bermudez

TL;DR –

April is one of the best times for West Kendall homeowners to review their insurance coverage before South Florida’s rainy season and hurricane season begin. Understanding homeowners’ insurance, flood insurance, roof-related considerations, and auto insurance coverage can help homeowners make informed decisions and better understand their available protection options before severe weather develops.

Why Should West Kendall Homeowners Review Their Insurance Before Hurricane Season?

Many West Kendall homeowners review their insurance before hurricane season because severe weather often exposes misunderstandings about coverage. Reviewing policies early provides an opportunity to understand available protections, policy limitations, deductibles, exclusions, and optional coverages before storms arrive.

Residents throughout South Florida know hurricane season arrives every year. Yet many homeowners wait until a tropical system appears on the forecast before reviewing their policies. By that point, questions about coverage, flood insurance, deductibles, and policy provisions suddenly become urgent.

The calmer months leading into hurricane season offer a much better opportunity to review coverage carefully, ask questions, and evaluate options without the pressure of an approaching storm.

What Does Homeowners Insurance Typically Cover?

One of the most common questions homeowners ask involves water damage.

The answer depends on the source of the water and the specific policy language.

Most standard homeowners insurance policies may provide coverage for certain sudden and accidental water-related losses, subject to policy terms, exclusions, limitations, and conditions. However, flood damage caused by rising water is generally treated differently and often requires separate flood insurance coverage.

Because policy language varies among carriers and policy forms, homeowners should review their individual policies carefully and consult a licensed insurance professional regarding their specific circumstances.

What Should Homeowners Know About Flood Insurance?

Flood insurance remains one of the most misunderstood insurance products in South Florida.

Many homeowners assume flood risk only exists within designated flood zones. However, flooding can occur in a variety of situations, including prolonged rainfall, overwhelmed drainage systems, and severe weather events.

Most standard homeowners’ insurance policies do not cover flood damage from rising water. As a result, many homeowners choose to explore separate flood insurance options.

Timing also matters.

Certain flood insurance programs may include waiting periods before coverage becomes effective. Homeowners interested in flood protection should review their options before severe weather becomes an immediate concern.

How Can Roof Maintenance Support Hurricane Preparedness?

Your roof serves as one of your home’s primary protective barriers.

Before hurricane season, homeowners may wish to:

- Inspect for visible damage

- Address maintenance concerns

- Repair loose or missing shingles

- Document the roof condition with photographs

Roof condition may be considered during underwriting and claims evaluations, depending on policy provisions, carrier guidelines, and the specific facts of a loss. Maintaining your property can help support overall preparedness efforts.

Why Review Auto Insurance Before the Rainy Season?

Rainy season affects more than homes.

Vehicles face increased exposure during periods of heavy rain, reduced visibility, and hazardous driving conditions.

A periodic auto insurance review provides an opportunity to better understand available coverages, liability limits, deductibles, and optional protections. Since every driver’s circumstances are unique, reviewing coverage periodically can help ensure policies continue to align with current needs.

Frequently Asked Questions

Does homeowners’ insurance automatically cover flooding?

Most standard homeowners’ insurance policies do not cover flood damage from rising water. Flood insurance is typically purchased separately through approved carriers and programs.

When should homeowners review insurance before hurricane season?

Many insurance professionals recommend reviewing coverage before hurricane season begins to allow time for planning, education, and evaluation of available options.

Can flood insurance be purchased when a storm is approaching?

Certain flood insurance programs may include waiting periods before coverage becomes effective. Availability and timing vary by carrier and program.

Why is April a good time for a policy review?

April allows homeowners to review their policies before South Florida’s rainy season and hurricane season create urgency and time constraints.

Should homeowners inspect their roofs before hurricane season?

Many homeowners choose to inspect and maintain their roofs before hurricane season as part of a broader storm preparedness strategy.

Compliance Disclaimer

This article is provided for educational and informational purposes only and should not be considered insurance, legal, financial, or regulatory advice. Coverage availability, terms, conditions, exclusions, limitations, endorsements, and pricing vary by carrier and policy. Please consult a licensed insurance professional regarding your specific insurance needs and business circumstances.

Insurance Disclosure

This article is provided for educational and informational purposes only and should not be considered insurance, legal, financial, or tax advice. Coverage availability, terms, conditions, exclusions, limitations, endorsements, waiting periods, and pricing vary by carrier and policy. Statements contained in this article are general in nature and may not apply to every individual, property, vehicle, or business situation.

Insurance coverage is subject to underwriting approval and policy terms. Homeowners, flood, auto, commercial, workers’ compensation, liability, and other insurance products may differ significantly among carriers. Readers should consult a licensed insurance professional regarding their specific insurance needs and circumstances before making any coverage decisions.

Del Toro Insurance and its representatives do not guarantee coverage, pricing, eligibility, claim outcomes, policy issuance, or future insurability. All insurance decisions should be based on a thorough review of policy documents and discussions with a qualified insurance professional.

{kind=link}